Andhra Pradesh BIEAP AP Inter 1st Year Accountancy Study Material 1st Lesson Book Keeping and Accounting Textbook Questions and Answers.

AP Inter 1st Year Accountancy Study Material 1st Lesson Book Keeping and Accounting

Short Answer Questions

Question 1.

Explain the advantages and limitations of Accounting.

Answer:

Advantages of Accounting: The following are the main advantages of accounting.

- Permanent and Reliable Record : Accounting provides permanent record for all business transactions and provides reliable information to different interested parties.

- Net Result of Business Operations: Accounting provides the final result (Profit or Loss) of business for a given period of time.

- Ascertainment of Financial Position: It is not enough to know only the profit or loss, but the proprietor requires a full picture of his financial position to plan for the next year’s business.

- Facility of Comparative Study: Accounting provides the facility of comparative study of the various aspects of the business such as profits, sales, expenses, etc.

- Control over Assets: In the course of business, the proprietor acquires various assets like building, machinery, furniture, etc. which are well protected by generating records.

Limitations of Accounting: The following are the limitations of Accounting.

- Records only monetary transactions : Accounting considers monetary transactions only, non-monetary transactions like quality, organization culture, units of production sales, etc. are ignored in accounting.

- Historical in nature : Accounting considers only historical transactions, i.e transactions which have occurred in the past only recorded in accounting books.

- Price level changes are not considered: Accounting does not consider price level changes which may occur from time to time, thus, it does not reflect the current position.

- Does not provide realistic information: While preparing the books of account, subjectivity of the accountant may influence the final results of the business enterprise. This may not provide realistic information which in turn affects the overall results of the business concern.

![]()

Question 2.

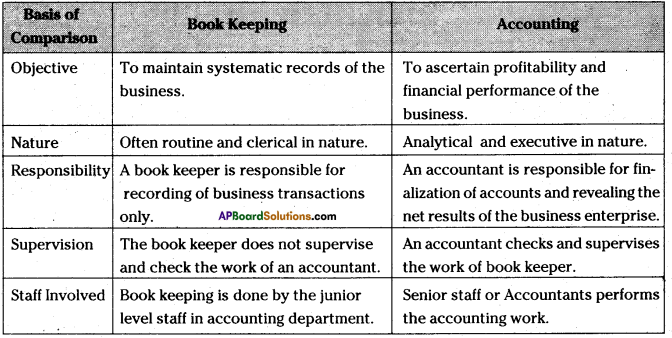

Distinguish between Book-keeping and Accounting.

Answer:

Question 3.

Explain the steps involved in Accounting process.

Answer:

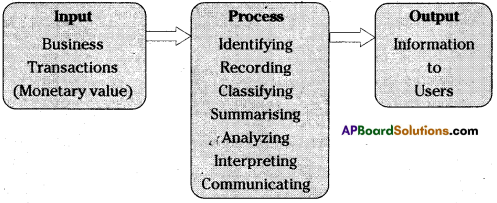

Accounting process:

- Identifying: Identifying the business transactions from the source documents.

- Recording: The next function of accounting is to keep a systematic record of all business transactions, which are identified in an orderly manner, soon after their occurrence in the journal or subsidiary books.

- Classifying : This is concerned with the classification of the recorded business transactions so as to group the transactions of similar type at one place.

- Summarizing : It is the process of finding the totals of balances of all accounts so as to prepare trial balance.

- Reporting : The classified information available from the trial balance is used to prepare – profit and loss account and balance sheet in a manner useful to the users of accounting

information. - Analysing: It establishes the relationship between the items of the profit and loss account and the balance sheet.

- Interpreting : It is concerned with explaining the meaning and significance of the relationship so established by the analysis. Interpretation should be useful to the users.

Very Short Answer Questions

Question 1.

What is Book-keeping ? (Mar. 2018 – A.P. ; Mar. ’17 – T.S. ; May ’17 – A.P. & T.S.)

Answer:

Book-keeping is the art of recording business transactions in a systematic manner. It covers four activities i.e. identifying the transactions, measuring the identified transactions, recording in a chronological order and classifying the recorded transactions.

Question 2.

Define Accounting. (Mar. 2019, ’17 – A.P.)

Answer:

The American Institute of Certified Public Accountants has defined the Accounting as “the art of recording, classifying and summarizing in a significant manner in terms of money transactions and events which in part, at least of a financial character and interpreting the results thereof”.

![]()

Question 3.

What is an Accounting cycle ? (Mar. 2018 – T.S. ; Mar. ’15 – A.P. & T.S.)

Answer:

An accounting cycle is a complete sequence beginning with the recording of transaction and ending with preparation of financial statements. It involves journalizing, ledger posting, balancing, trial balance, preparation of trading, profit and loss account and balance sheet.

Student Activity

- Goto nearest business organizations and observe the book keeping and accounting systems adopted by them.

- Observe the accounting procedures adopted by large size or medium size organizations located nearby them.