Andhra Pradesh BIEAP AP Inter 1st Year Accountancy Study Material 11th Lesson Rectification of Errors Textbook Questions and Answers.

AP Inter 1st Year Accountancy Study Material 11th Lesson Rectification of Errors

Short Answer Questions

Question 1.

Give two examples of Errors of Omission.

Answer:

When a transaction is completely or partly omitted from the books of accounts such error is known as Error of Omission.

- When no entry is made for a transaction in journal

E.g.: Purchase of goods are not recorded in the books of original entry. - If an entry is not made for a transaction in the Subsidiary Book

E.g.: Paid cash to Ganesh traders not entered in Cash Book.

Question 2.

Explain the errors of commission with two examples.

Answer:

The errors arise due to wrong recording, wrong posting, wrong casting, wrong entry forwarding, wrong balancing, etc.

- Wrong recording: When a transaction is incorrectly recorded in the books of original entry E.g.: Slaes of goods to Rama of Rs. 150 recorded as Rs. 50.

- Wrong casting : If the mistake is committed in totaling, it is called error of commission.

E.g.: Sales book is overcast by Rs. 100.

![]()

Question 3.

Explain the errors of Principle with two examples.

Answer:

Errors which are committed by violating or defective knowledge of accounting principles (rules). These errors may arise, when the clear distinction is not made between the Capital and Revenue nature items.

E.g.:

- Purchase of land & buildings – debited to purchases a/c instead of land & buildings a/c.

- Rent paid to landlord – debited to landlord a/c instead of rent a/c.

Question 4.

Explain the compensating errors. (Mar. 2018 – A.P.)

Answer:

If two or more errors are arised and one error nullifies the another error, the net effect is unchanged, these are Called compensating errors.

E.g.: Amount paid to Teja Rs. 2000 recorded as Rs. 200 and Amount received from Krishna Rs. 10,000 recorded as Rs. 9,500.

Question 5.

Define suspense account.

Answer:

Sometimes, despite an accountant’s best efforts, the trial balance may not agree. In such circumstances, the differnce between the debit and credit Totals should be transferred to an account called Suspense Account. It is an imaginary account, opened and used as a temporary measure to make two sides of the trial balance agree.

Essay Type Questions

Question 1.

What are the various types of errors ? Explain. (Mar. 2018 – A.P. – May ’17 – A.P. & T.S.; Mar. 17. ’15 – T.S.)

Answer:

Errors may be classified as:

1) Errors of Principle

2) Errors of Omission

3) Errors of Commission

4) Compensating Errors

5) Writing to wrong head of account

1) Errors of Principle : Errors which are committed by violating or defective knowledge of accounting principles (rules). These errors may arise, when the clear distinction is not made between the Capital and Revenue nature items.

E.g.:

- Purchase of land & buildings – debited to purchases a/c instead of land and buildings a/c.

- Rent paid to landlord – debited to landlord a/c instead of rent a/c.

2) Errors of Omission : When a transaction is completely or partly omitted from the books of accounts such error is known as Error of Omission.

- When no entry is made for a transaction in journal

E.g.: Purchase of goods are not recorded in the books of original entry. - If an entry is not made for a transaction in the Subsidary Book E.g.: Paid cash to Ganesh not entered in Cash Book.

3) Errors of Commission : The errors arise due to wrong recording, wrong posting, wrong casting, wrong entry forwarding, wrong balancing, etc.

- Wrong recording : When a transaction is incorrectly recorded in the books of original entry E.g.: Sales of goods to Rama of Rs. 150 recorded as Rs. 50.

- Wrong Casting : If the mistake is committed in totaling is called error of commission. E.g.: Sales book is overcast by Rs. 100.

4) Compensating Errors: If two or more errors are arised and one error nullifies the another error, the net effect is unchanged, these are called compensating errors.

E.g.: Amount paid to Teja Rs. 2000 recorded as Rs. 200. and amount received from Krishna Rs. 10,000 recorded as 9,500.

5) Writing to wrong head of account: Instead of recording one account, recording another account is known as writing to wrong head of a/c.

E.g.: Paid to Vijay Rs. 1,000 is debited to Vinay a/c.

![]()

Question 2.

What are the errors disclosed by Trial Balance and not disclosed by Trial balance ? (Mar. 2019 – A.P. & T.S.)

Answer:

Errors may be classified as

I) Errors not disclosed by Trial Balance

II) Errors disclosed by Trial Balance .

I) Errors not disclosed by trial balance :

- Errors of Principle

- Errors of Omission

- Errors of Commission

- Compensating Errors

- Writing to wrong head of account

II) Errors disclosed by Trial Balance :

- Posting of transaction to wrong side of an account

- Posting of wrong amount to an account

- Errors in totaling

- Errors of carrying forward

- Posting of only one aspect of journal entry into ledger

- Recording one aspect twice

Question 3.

What is meant by Suspense Account? Why Is It opened ?Explain. (Mar. ’17, ’15 – A.P.)

Answer:

Sometimes, despite an accountant’s best efforts, the trial balance may not agree. In such circumstances, the difference between the debit and credit Totals should be transferred to an account called ‘Suspense Account’. It is an imaginary account, opened and used as a temporary measure to make two sides of the trial balance agree.

The suspense account may show any balance, suspence account will be written off after the errors are detected and rectified. If the opening balance of suspense a/c is not given, the difference of suspense account is to be considered as opening balance.

Problems

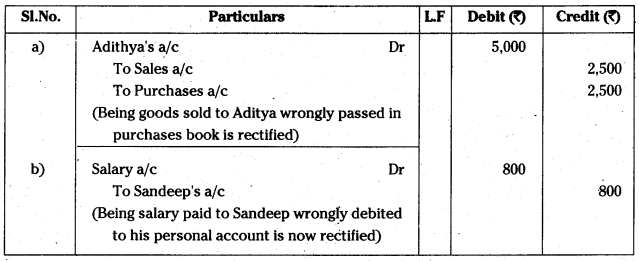

Question 1.

Rectify the following errors:

a) A sale of goods to Adithya for Rs. 2500 was passed through the purchases book.

b) Salary of Rs. 800 paid to Sandeep was wrongly debited to his personal account.

c) Furniture purchased on credit from Sekhar for Rs. 1000 was entered in the purchases book.

d) Rs. 5000 spent on the extension of buildings was debited to buildings repairs account.

e) Goods returned by Shailesh Rs. 1200 were entered in the Return Outwards book.

Answer:

Rectification Entries

![]()

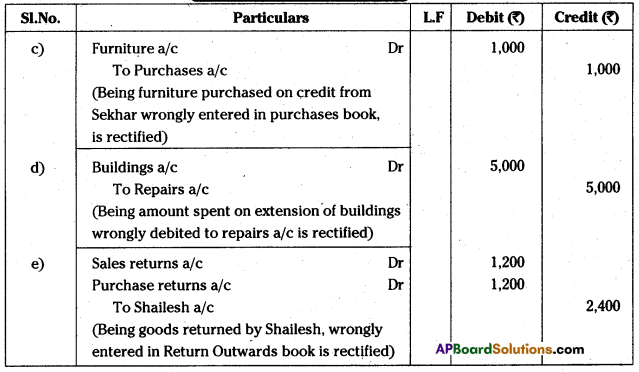

Question 2.

Rectify the following errors;

a) Furniture purchased for Rs. 10,000 wrongly debited to purchase account.

b) Machinery purchased on credit from Ramana for Rs. 20,000 was recorded through purchases book.

c) Repairs on machinery Rs. 1,400 debited to machinery account.

d) Repairs on overhauling of secondhand machinery purchased Rs. 2,000 was debited to repairs account.

e) Sale of old machinery at book value of Rs. 3,000 was credited to sales account.

Answer:

Rectification Entries

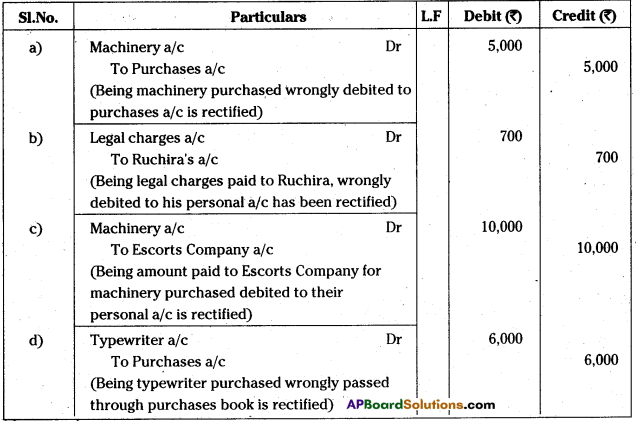

Question 3.

Pass journal entries to rectify the following errors:

a) Machinery purchased for Rs. 5,000 has been debited to purchases a/c.

b) Rs. 700paid to Ruchira as legal charges were debited to his personal account.

c) Rs. 10,000 paid to Escorts Company for machinery purchased stand debited to Escorts company account.

d) Typewriter purchased for Rs. 6,000 was wrongly passed through purchase book.

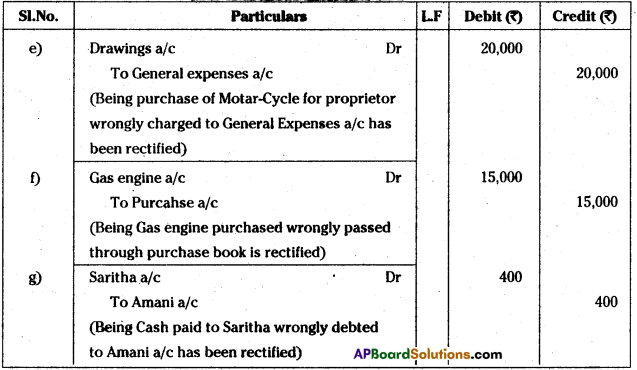

e) Rs. 20,000 paid for the purchase of Motor-Cycle for proprietor has been charged to General Expenses’a/c.

f) Rs. 15,000 paid for the purchase of Gas engine’ were debited to ‘Purchases’ a/c.

g) Cash paid to Saritha Rs. 400 was debited to the account of Amani.

Answer:

Rectification Entries

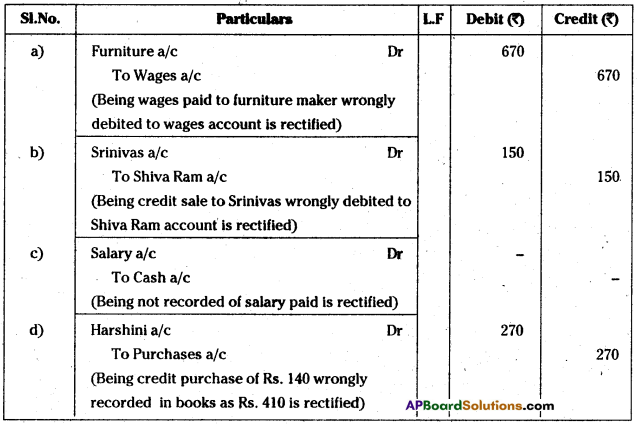

Question 4.

Give rectification entries for the following errors:

a) Wages payable to furniture maker Rs. 670 debited to Wages a/c.

b) A credit sale of Rs. ISO to Srinivas debited to Shiva Ram.

c) Payment of salary to Varshini not passed through books at all.

d) A credit purchase ofRs. 140 to Harshini, recorded in the books as Rs. 410.

Answer:

Rectification Entries

![]()

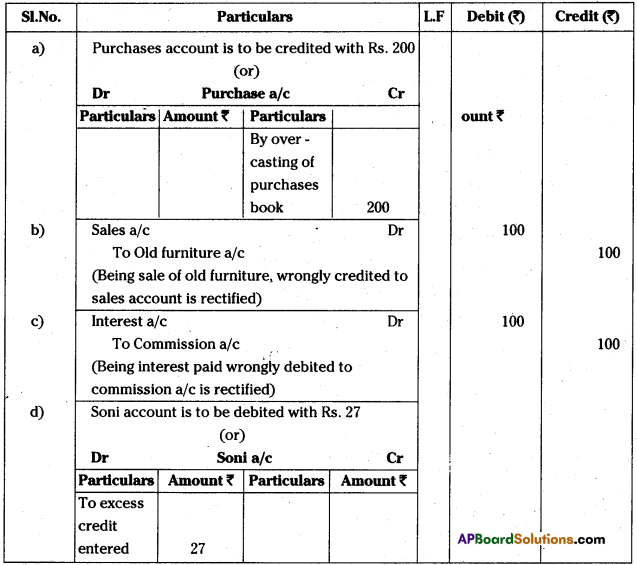

Question 5.

Pass journal entries to rectify the following errors:

a) The purchases book of the trader is overadded by Rs. 200. (Overcast by)

b) Old furniture sold for Rs. 100 was wrongly credited to sales a/c.

c) Rs. 100 paid on account of interest was debited to commission account.

d) An amount of Rs. 125 received from Soni was wrongly credited to his account as Rs. 152.

Answer:

Rectification Entries

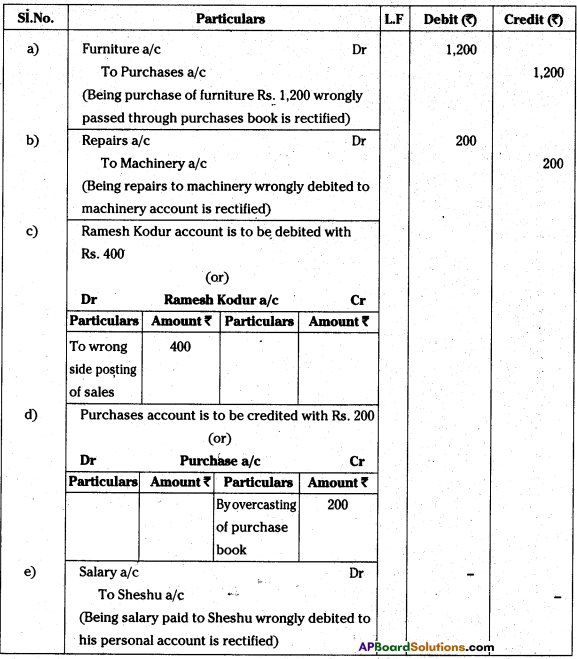

Question 6.

Rectify the following errors:

a) Purchases of furniture costing Rs. 1,200 have been passed through purchases book.

b) Repairs to machinery Rs. 200 were debited to machinery account.

c) A credit sale ofRs. 200 to Ramesh Kodur through properly entered in the sales book has been credited to his account.

d) The total of purchases book, was overcast by Rs. 200.

e) Salary paid to Sheshu, manager stands debited to his account.

Answer:

Rectification Entries

Question 7.

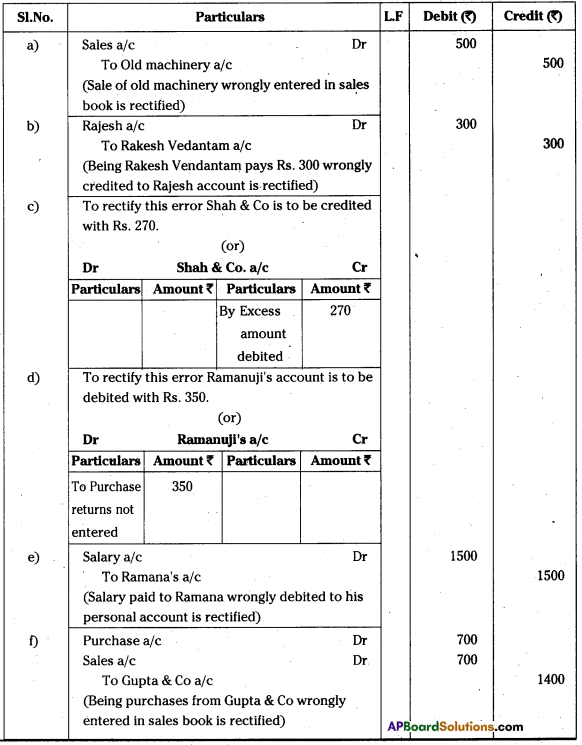

Rectify the following errors:

a) Sale of old machinery Rs. 500 has been entered in the sales book.

b) Rakesh Vedantam pays 300. This amount has been credited to Rajesh.

c) A sale ofRs. 250 to Shah & Co., has been debited to them as Rs. 520.

d) Returns to Ramanuji Rs. 350 have not been posted to his account.

e) Salary of Rs. 1500 paid to Ramana has been debited to his account.

f) A purchase ofRs. 700 from Gupta & Co., has been entered in the sales book.

Answer:

Rectification Entries

![]()

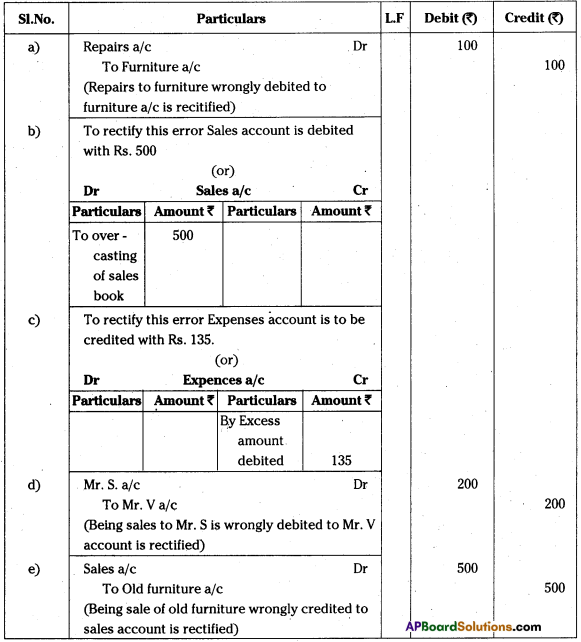

Question 8.

Rectify the following errors:

a) An amount of Rs. 100 paid for the repairs of furniture was debited to furniture account,

b) Sales book total was overcast by Rs. 500.

c) Expenses 15 were posted in the ledger as 150.

d) A sale ofRs. 200 to Mr. S. was wrongly debited to the account of Mr. V.

e) Old furniture sold has been credited to sales a/c Rs. 500,

Answer:

Rectification Entries

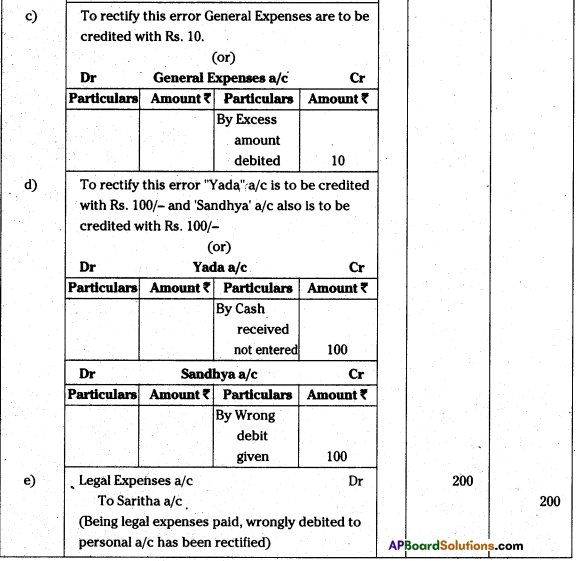

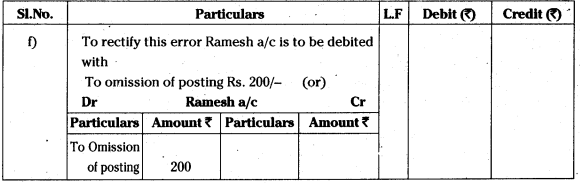

Question 9.

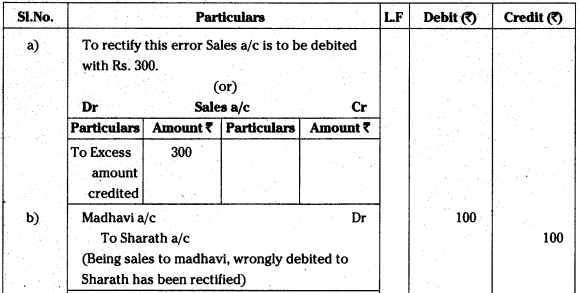

Write the entries for the rectification of the following errors:

a) Sales book was overcast by Rs. 300.

b) Sales of Rs. 100 to Madhavi was wrongly debited to account of Sharath.

c) General expenses of Rs. 20 were posted in the general ledger as Rs. 30.

d) Rs. 100 received from Yada was debited to Sandhya.

e) Legal expenses Rs. 200 paid to Saritha was debited to her personal account.

f) An amount of Rs. 200 paid of Ramesh is not posted to his account.

Answer:

Rectification Entries

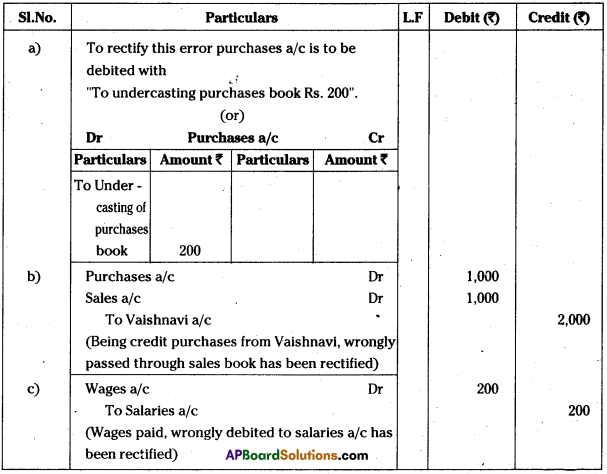

Question 10.

Pass Journal en fries for rectification of the following errors:

a) The total of purchases book was undercast by Rs. 200.

b) A credit purchase from Vaishnavi for Rs. 1000 has been wrongly passed through the sales book

c) Wages paid Rs. 200 was wrongly debited to salaries account.

d) Rs. 100 receIved on account interest stands wrongly credited to commission account.

e) Salary of Rs. 500 paid to manager Mr. Krishna (s debited to his personal account.

Answer:

Rectification Entries

Question 11.

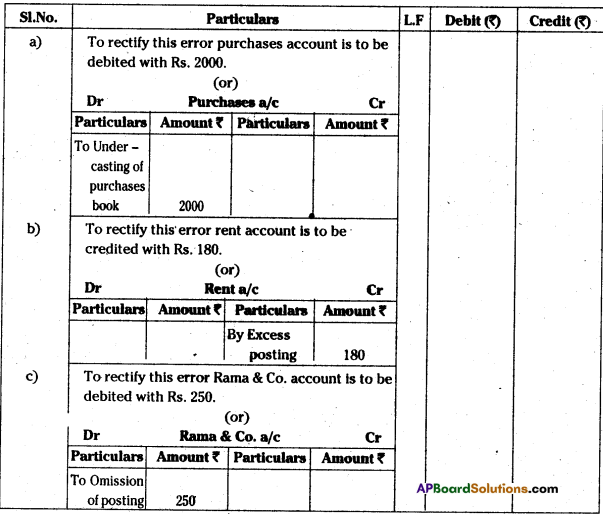

Rectify the following errors before preparation of trial balance:

a) Purchase book was undercast by Rs. 2000.

b) Rent paid Rs. 350 was debited to that account as Rs. 530.

c) Discount received from Rama & Co. Rs. 250 was not posted to their account.

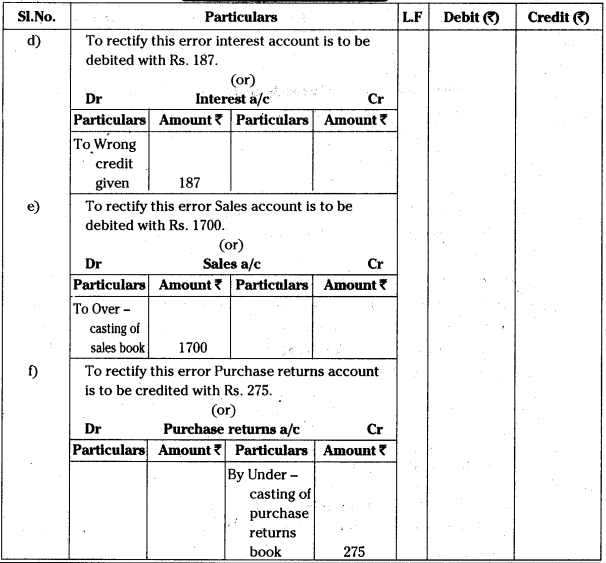

d) Interest paid Rs. 89 was wrongly credited to that account as Rs. 98.

e) Sales book was overcast byRs. 1700.

f) Purchase returns book undercast by Rs. 275.

Answer:

Rectification Entries

Question 12.

Rectify the following errors discovered before preparation of the trial balance.

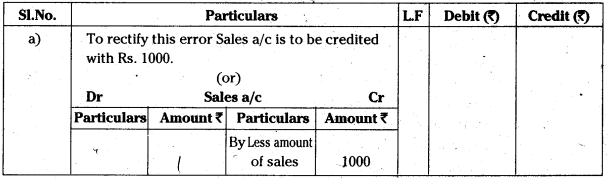

a) The sales book has been totaled Rs. 1000 short.

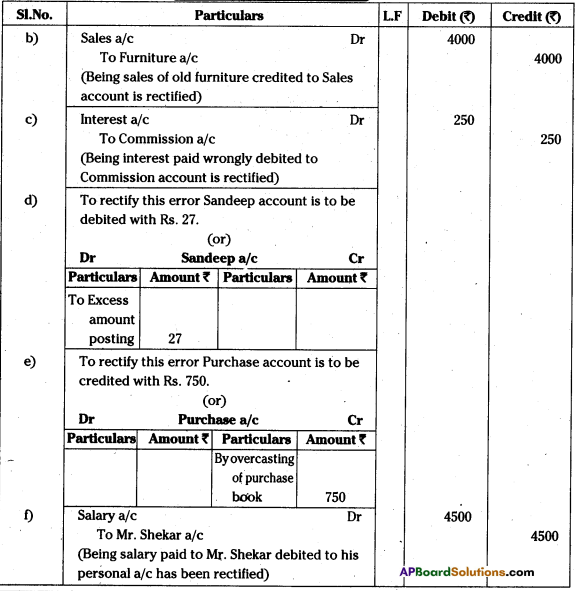

b) Sale of old furniture Rs. 4000 was credited to sales account.

c) Rs. 250 paid towards interest was debited to commission account.

d) Rs. 125 paid by Sandeep but was entered in his account Rs. 152.

e) The purchase a/c was overcast by Rs. 750.

f) Rs. 4500 salary paid to Mr. Shekar head clerk stands debited to his personal account.

Answer:

Rectification Entries

![]()

Question 13.

Rectify the following errors dicovered before preparation of the trial balance.

a) Furniture purchased Rs. 3,500 has been passed through the purchases book.

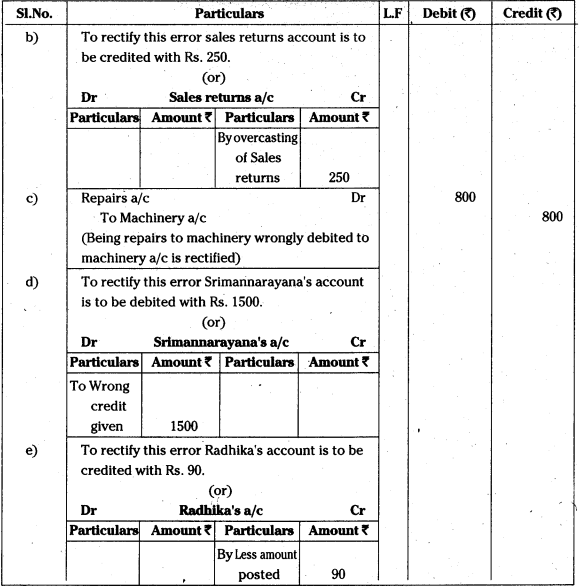

b) The returns inward book was overcast by Rs. 250.

c) Rs. 800 paid for repairs to machinery was debited to machinery account

d) A sale ofRs. 750 made to Srimannarayana was entered in sales book but was credited to his account.

e) A purchase ofRs. 760 made from Radhika was credited to his account Rs. 670.

Answer:

Rectification Entries

Question 14.

Rectify the following errors before preparation of trial balance.

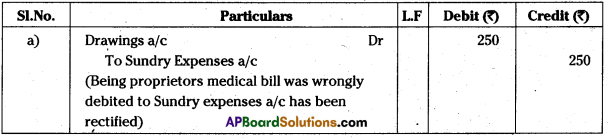

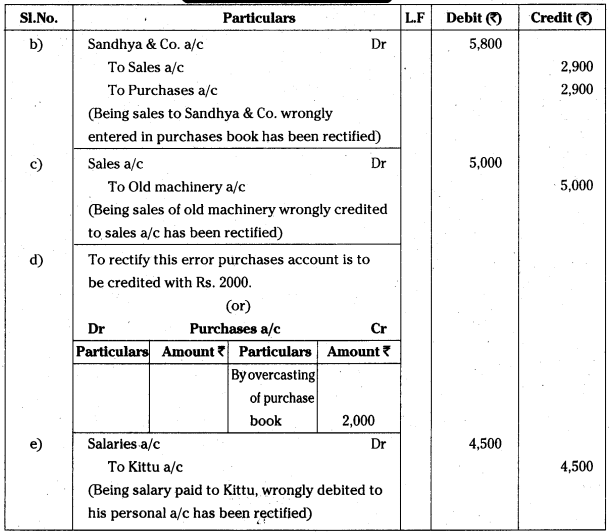

a) Rs. 250paid for proprietors medical bill was debited to sundry expenses account.

b) Sale of goods to Sandhya & Co. for Rs. 2900 was entered through the purchase book.

c) Sale of old machinery Rs. 5000 was posted to the credit of sales account.

d) The total of purchase book was overcast by Rs. 2000.

e) Salary ofRs. 4500 paid to Kittu has been debited to his account.

Answer:

Rectification Entries

Question 15.

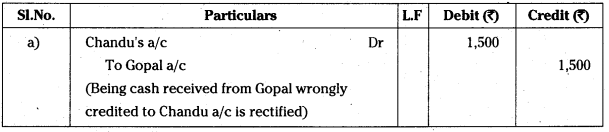

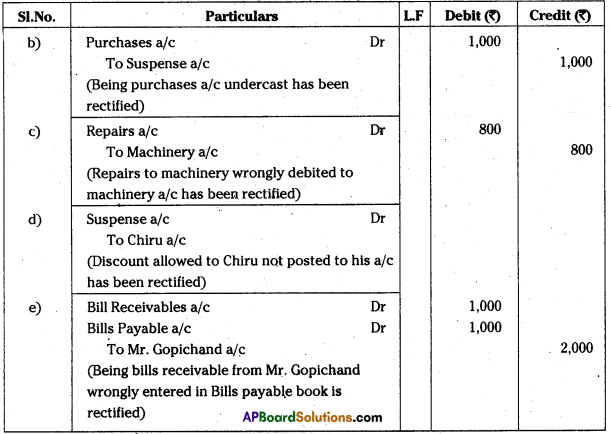

Pass necessary entries to rectify the following errors. After the preparation of trial balance.

a) Rs. 1500 received from Gopal has been wrongly credited to Chandu’s a/c.

b) The purchase book was undercast by Rs. 1000.

c) Repairs to machinery Rs. 800 were debited to machinery account.

d) Discount allowed to Chiru Rs. 200 correctly entered in cash book, has not been posted to his account.

e) Bills payable from Mr. Gopichand Rs. 1000 was entered in the bills payables book.

Answer:

Rectification Entries

Student Activity

Visit any small organisation and note down its experiences in rectifying the errors.