Students can go through AP State Board 9th Class Social Studies Notes Chapter 9 Credit in the Financial System to understand and remember the concept easily.

AP State Board Syllabus 9th Class Social Studies Notes Chapter 9 Credit in the Financial System

→ Banks accept deposits that can be withdrawn at any moment They work under the R.B.I. Banks honor withdrawals in cash and cheques.

→ Banks in India keep 15% of their deposits as cash to repay the depositors. Bank uses the major portion of the deposits to extend loans.

→ Bank charges interest on loans. The difference between what is charged from borrowers and what is paid to depositors is the primary source of income for banks.

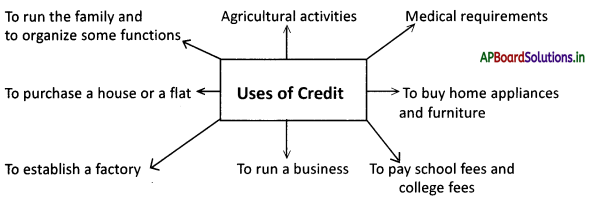

→ There are many reasons for taking credit A large number of transactions in our day-to¬day activities involve credit in some form or the other.

→ Interest rates, collateral and documentation requirement, and the mode of repayment together comprise what is called the terms of credit

→ There are two types of sources of credit One formal and the other informal.

→ Banks and cooperatives come under formal sources of credit The informal lenders are moneylenders, traders, employers, relatives, and friends,

→ Informal sources of credit are the reason for rural indebtedness.

![]()

→ Self-help groups give loans to the rural poor especially women without collateral and documentation. They save women from the exorbitant interest rates of money lenders. Group members are jointly responsible for the repayment of loans. These loans created self-employment and made women self-reliant

→ Demand deposits Since the deposits in the bank can be withdrawn on demand, these deposits are called demand deposits.

→ Economic activities: All the activities that deal with money involving – production, industrial activities, and trading activities, and other purposeful activities are called economic activities.

→ Cooperative societies: A business or organization owned equally by all the people working in the field, i.e. agriculture or mining or handlooms, etc.

→ Commercial banks: All institutions that accept deposits and lend loans and work under the regulations of the Reserve Bank of India are called commercial banks.

![]()

→ Informal sources of credit: All the people, who do not follow any rules and regulations in issuing loans together are called informal sources of credit. e.g.: Moneylenders, traders, friends, relatives, etc.

→ New Initiatives: The RBI has been taking steps for improving the financial access to people in rural areas. Banks operate in rural areas either through branches or through Business Correspondents (BCs). A Business Correspondent is an approved bank agent providing basic banking services using a Micro ATM (terminal). These Business Correspondents encourage people in rural and remote areas to open bank accounts, save money and also use loan facilities provided by the banks. Bio-metric smart card identification systems are used to open these accounts.

→ Aadhaar Enabled Payment System (AEPS):

- AEPS is a new payment service offered by the National Payments Corporation of India (NPCI) to banks, financial institutions using the ‘Aadhaar’ number and online UIDAI authentication through their respective Business Correspondent service centers.

- The customer needs his / her bank account linked to their Aadhaar number with the bank offering the AEPS service.

- A customer can at present avail of the following four services using AEPS through the micro – ATMs at BCs :

(a) Cash Withdrawal

(b) Cash Deposit

(c) Balance Enquiry

(d) Fund transfer

→ Financial Literacy: Financial Literacy is the process of equipping oneself with knowledge and information on financial matters. Taking interest in financial literacy helps one to have better financial planning, puts them in a better position to achieve their financial goals, and protect themselves from frauds and debt traps. It aims to inculcate savings habits, improve the understanding of financial products leading to effective use of financial services, and thus helps better money management. Further, financial literacy facilitates easy access to financial services.

Financial literacy material is available on the website of the Reserve Bank of India (www.rbi.org.in).

→ The financial literacy material available now covers subjects such as features of genuine banknotes, know your Reserve Bank, how RBI touches the life of the common person, caution against emails/ SMS offering huge sums of money from abroad, caution against providing bank account details on the internet, information of loan products available from banks, why save with banks ?, grievance redressal mechanism, Banking Ombudsman Scheme, caution against depositing money in unincorporated bodies/ unlicensed entities, Deposit Insurance (Are my deposits safe in banks ?, What is Deposit Insurance and Credit Guarantee Corporation), etc.

→ Financial literacy information is available in brochures/pamphlets prepared by RBI and other banks. Further, RBI has developed com¬ics on financial literacy subjects for the benefit of the school children. ‘Raju and the Money Tree’, ‘Money Kumar and Monitory Policy’ etc., are the names of the comics that can be downloaded from the RBI website mentioned above. In addition to the above, for the ben¬efit of word illiterate persons in rural, urban and remote areas, the State Level Bankers Committee (SLBC), Andhra Pradesh has prepared an audio CD on the benefits of saving with banks.

→ Financial Literacy is an important adjunct for promoting financial inclusion, consumer protection, and ultimately financial stability. Financial inclusion and financial literacy need to go hand in hand to enable the common man to understand the need and benefits of the products and services offered by formal financial institutions. In India, the need for financial literacy is even greater considering the low levels of literacy and the large section of the population that are still out of the formal financial setup. Financial literacy has assumed greater importance in recent years as financial markets have become increasingly complex and the common man finds it very difficult to make informed decisions. Further, in view of a higher percentage of household savings in our country, financial literacy can play a significant role in the efficient allocation of household savings and the ability of individuals to meet their financial goals.